1300 38 66 34

1300 38 66 34

SO WHAT SHOULD YOU DO NOW?

Whilst the country tuned in for the 2020 Melbourne Cup, the cash rate decision for November was announced and rates have been cut.

In response to the economic impact being caused by the COVID-19 crisis, the RBA reduced the cash rate by 0.15% to a new record low of 0.1%.

Let's be clear - The RBA wants you to do your bit for Australia and start spending, but is this necessarily the best thing for you?

How to really capitalise

In making this change the RBA has confirmed the views of many analysts that further stimulus is required to aid Australia's recovery post Covid. It had previously stated that it sees a cash rate of 0.25% as a floor however it has softened its stance on a reduction more recently.

In the lead up to its next meeting, our central bank will continue to monitor world events such as the second round of European lockdowns and the outcomes of US election, while closer to home it will be hoping the easing of restrictions in Victoria and the opening of state borders will provide a lift to the economy.

As you're probably aware, lenders review rates independently of the RBA and some may decide to pass this rate decrease on to customers at different levels over varying time frames.

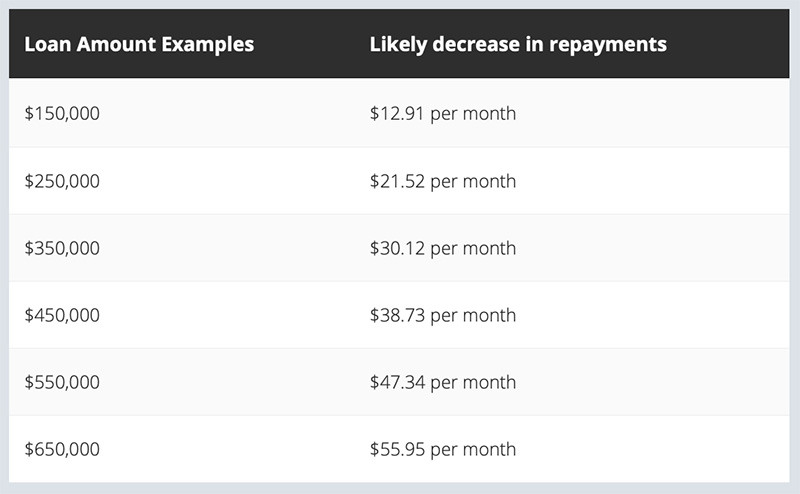

Meanwhile here is a table showing how Australia's average mortgage sizes may be affected:

OPTIONS

NEW BORROWING

In current economic climate are you able to borrow from the banks and lenders at good interest rates? If you are able to borrow

1. Make sure any property you are considering has solid reliable and strong income streams and certainties of tenancy.

2. Look at the yield deloivery from rental income returns. Make sure they are significant and long into the future

3. Look at certainty and length of tenancy. You do not want to 'worry' about tenancy turnover, creating unwanted pressure of servicing any borrowing.

What's the best solution? We believe the best way to secure substantial rental incomes is through ownership of NDIS / SDA properties. Get insights to NDIS / SDA properties here. The yields from rental income returns are significant - yield is always subject to cost of ownership, but over 10% yield is considered very conservative and below normal for this asset class.

EXISTING BORROWING

1. Don’t do a thing.

If your home loan is variable, your existing lender should reduce the rate of interest you’re being charged and give you the option of reducing your repayments accordingly. The money you’re saving is what the RBA wants you to start putting into the economy to help give it the boost it needs. So, if you’re thinking of buying yourself something special, at least you can tell yourself "you’re doing it for everyone":)

Article in The Australian just days ago suggested the following 7 words as being, extraordinarily powerful with banks and lenders. " I am considering signing a discharge authority ".

Literally that is said to cut through the noise, as it is 'banking language' and is putting your lender on notice that you are considering changing lenders, subject to what they say in response.

2. Lock in a fixed rate

You can choose to fix all or part of your loan, and “lock in” a low interest rate. A fixed rate loan can provide security in terms of being able to budget cash flow. It can also provide protection when rates are rising. However, in the current climate of falling rates, it can be tricky to get the timing right. There are a few tools that can help, although there will always a degree of uncertainty when trying to predict the movement of interest rates.

Regardless of whether you get the timing ‘right’ (and you won’t know this until after the fixed period has ended), you need to make sure you select a fixed loan for the right reasons.

3. Start shopping around.

You’ve probably seen in the news that some lenders aren’t passing the full cuts onto their customers. If you’re not happy with your bank’s rate it’s a good time to shop around for a loan from a lender that has passed on all the rate drops. It’s important to review and compare your loan on a regular basis, so please get in touch to make a time to review your current situation.

4. Keep your repayments the same.

If you’re comfortable with what you’ve been used to paying, keep paying it. With your required repayments being lower, you’ll be paying off more of the principal with every payment. Not only will that reduce the amount your interest is charged on (reducing your required repayments even further), it means you’ll take months or years off your loan.

5. Save the money.

With rates this low, you’d have to think it’s inevitable they’ll go up one day. Rather than making extra payments you can choose to put the extra cash into savings to build a buffer for any future rises.

There are smarter ways than simply putting money into a basic savings account. Many loans have a redraw facility which lets you put extra payments into a loan, reducing the principal and interest, and allowing you to take out the extra money if and when you need it.

Or there is an offset account – a separate account that’s linked to your loan. Any money in this account will reduce the amount of the loan that interest is calculated on, but the funds are always available for your use if you want them. Even having your salary paid into an offset account will help reduce your interest charges for the time the money is in the account.

6. Pay off other debt.

Now is a great time to pay off that car loan or credit card that’s attracting higher interest rates than your home loan. Not only will you be reducing your debt, you’re also improving your financial position in the eyes of a lender, which is important if you’re thinking of refinancing or borrowing more to buy your next home.

7. Invest in a holiday.

Maybe your payments have forced you to sacrifice doing some of the things you’ve always wanted. Now might be a nice time to consider making a personal investment in some domestic aeroplane tickets, and keep the RBA happy by keeping your travels inside Australia.